The Bond Market Is the Boss

Everyone on Wall Street has the same story. Rising global bond yields? Blame Iran. Energy import costs, inflation fears, central banks with their hands tied. The narrative is clean, it makes for good headlines, and it gets clicks.

But the market structure is saying something completely different. If you’ve been following these pages, you know there’s a rumbling that you can hear in the distance that is approaching.

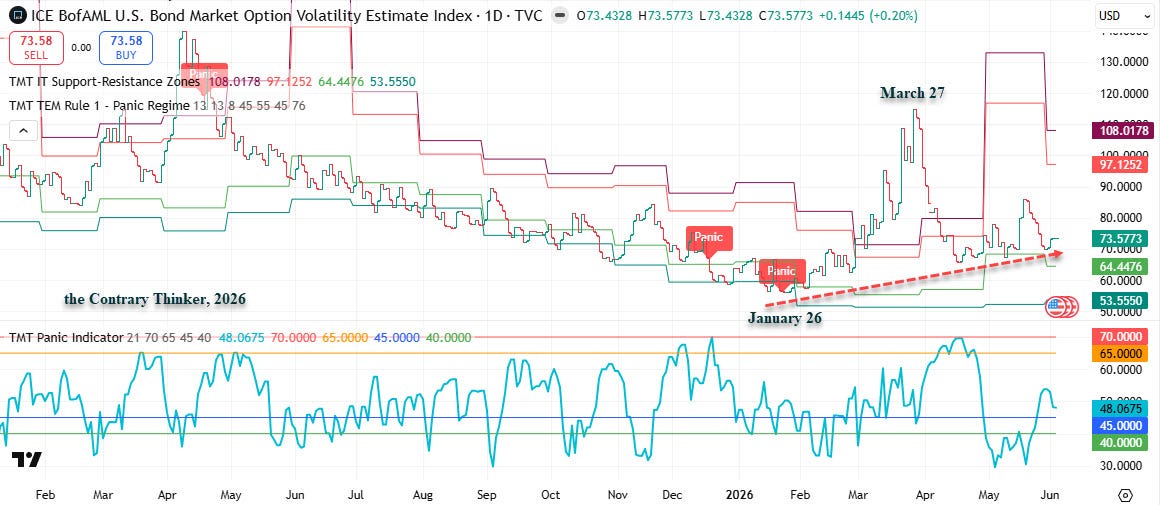

Perceived fear of owning risk assets was quietly increasing from the start of 2026, months before the crisis between Iran and the United States. Both the World Bond Index Fund we demonstrated yesterday and the 30-year UK Government Bond were showing risk aversion well before any military engagement. The pros on Wall Street, no matter what side of the desk they sit on, treat volatility as something to shrug off and spin. It is chronically used as a hedging tool, a premium tool, a short volatility tool, and nothing more. That reflex is going to cost them, in a massive of short cover.

The inflation everyone is pointing to is a byproduct of a geopolitical context we have been laying out for months. It is structural and geopolitical, not cyclical. It is a hybrid. It is anti-fragile. It resists the usual policy tools because it does not come from the usual places. It is not the cause of what is coming. The cause is a credibility crisis, and credibility is the reason we are heading toward a spike in volatility, hyper-correlation, and a structural repricing that the consensus is not prepared for.

“The concept of diversification is the foundation of modern portfolio theory. Like a wizard, the financial engineer is somehow able to magically reduce the risk of a portfolio by combining anti-correlated assets. The theory failed spectacularly in the 2008 crash when correlations converged. You can never destroy risk, only transmute it. All modern portfolio theory does is transfer price risk into hidden short correlation risk. There is nothing wrong with that, except for the fact it is not what many investors were told, or signed up for.”

— Christopher Cole,

The war is only one small piece of it. Add the $177 billion slush fund the president created to distribute to allies, now thrown out by the deputy at the DOJ but highlight the intent. Add what looks like active trading on inside information from the highest office in the land. Those are simply the icing on the cake. The cake itself is a fiscal mess with zero discipline and no exit.

Or rather, the traditional exit being mentioned is to print money and inflate your way out of it. I’ll come back to that notion.

And it is not just the United States. Japan, which we highlighted in the monthly MarketMap™, is using currency intervention instead of rate hikes as a monetary tool to control inflation. All while running a massive fiscal stimulus program. Same disease, different symptoms.

Here is the key. When it comes to bond investing, it all boils down to institutional trust: the credibility of political leadership, the quality of the fiscal framework, and the geopolitical context of the world, which has systematically shifted from the American century to something fractured, volatile, and ungoverned by norms.

The paper of the United States is no different from the paper issued by France, Germany, China, or any emerging market. They are all viewed the same way now. How do the institutions behind those pieces of paper hold up? Are the central banks truly independent? Is there a durable fiscal framework that does not change (day trade) week to week to manipulate markets? Are the political systems of the issuing nations acting in the long-term interest of their citizens?

The people in the institutions that fund the debt, the bond market, are asking these questions. And the answers, across developed countries around the world, are eroding. Independent central banks, durable fiscal frameworks, political systems acting in the public interest: these are the conditions that underwrite the risk premium. As they erode, the premium erodes with them.

That is the story the headlines are missing. Iran is the excuse. Credibility is the cause. “the ContraryThinker™ expects an unexpected shock to the system, something out of left field. The train that nobody sees rumbling toward them. That will be the catalyst that kicks off the next volatility spike and the hyper-correlation where there is no place to hide.

Anyone with an internet connection can drown in forecasts, charts, and market analysis by breakfast, and all of it costs exactly what it’s worth.

What nobody gives away is the call before the move, the lens that has caught the tops and bottoms the herd missed for 37 years. Become a MarketMap™ subscriber and you will never be the last one to know.